Selling goods to other EU countries

As a general rule, you must charge VAT on your sales when you sell goods to a buyer in another EU country. In some cases, you must sell the goods exclusive of VAT. Normally the buyer is then required to report the VAT in the other EU country instead.

Here are some examples of the most common scenarios, and the most important things for you to consider when selling goods to buyers in other EU countries

Selling goods exclusive of VAT within the EU

If your business sells goods to buyers in other EU countries, there may be circumstances in which you must not charge VAT on your sales. Some specific requirements must be fulfilled for you to sell goods exclusive of VAT in this way.

The buyer must be registered for VAT in an EU country other than Sweden and must provide you with details of their valid VAT number when making their purchase. The goods must also be transported from Sweden to another EU country. As the seller, you must have documentation confirming that the goods have been transported, regardless of who was responsible for transporting them. You can read more about this below under the headings “If the seller is responsible for transport” and “If the buyer is responsible for transport”.

If you have made a VAT-exclusive sale of goods to a VAT-registered buyer in another EU country, you must report this sale in your Swedish VAT return. You must also submit an EC sales list (recapitulative statement) containing details of the buyer’s VAT number and the amount you sold the goods for.

The details you provide in your EC sales list will enable the tax authority in the other EU country to verify that the buyer’s VAT reporting on their purchase is accurate.

A VAT-exclusive sale to a VAT-registered buyer in another EU country is also known as “intra-Community selling”. Correspondingly, the buyer’s purchase is sometimes referred to as an intra-Community acquisition.

If the seller is responsible for transport

To sell goods exclusive of Swedish VAT, you must be able to provide evidence that the goods have been transported from Sweden to another EU country. A shipping invoice and a transport document may be sufficient proof.

You can also choose to apply the presumption rule, which is optional. Under this rule, it is assumed that the goods you have sold have been transported to another EU country, if you can provide the specific documents required.

Presumption rule: when the seller is responsible for transportation

As the seller, you must be able to present at least two documents showing that the goods have been transported to another EU country if you are responsible for their transportation. These documents must have been issued by two independent parties. These parties must also be independent of both you and your buyer, which means that they must have no family ties to either of you, for example.

To prove that the goods have been transported from Sweden to another EU country, you must be able to present at least two transport documents.

Examples of transport documents

- a signed CMR document

- a signed consignment note

- a bill of lading (often used for sea transport)

- an invoice issued by the goods transport company.

Alternatively, you can present one transport document and one of the following documents:

- an insurance policy relating to the dispatch or transportation of the goods, or banking documents confirming payment of transport or delivery of the goods

- official documents issued by a government agency confirming arrival of the goods in the EU country to which they were transported.

- a receipt issued by a stockist in the EU country to which the goods were transported, confirming storage of the goods in that country

Please note that you cannot apply the presumption rule if you transport the goods to another EU country using your own means of transport, such as your private car.

Application of the presumption rule is optional, so it does not prevent you from using other documentary proof of transport.

If the buyer is responsible for transport

To sell goods exclusive of Swedish VAT, you must be able to provide evidence that the goods have been transported from Sweden to another EU country. A shipping invoice and a transport document may be sufficient proof.

You can also choose to apply the presumption rule, which is optional. Under this rule, it is assumed that the goods you have sold have been transported to another EU country, if you can provide the specific documents required.

Presumption rule: when the buyer is responsible for transport

As the seller, you must be able to present at least two documents proving that the goods have been transported to another EU country, even in cases where the buyer is responsible for transport. These documents must have been issued by two independent parties. These parties must also be independent of both you and your buyer, which means that they must have no family ties to either of you, for example.

To prove that the goods have been transported from Sweden to another EU country, you must be able to present at least two transport documents.

Examples of transport documents

- a signed CMR document

- a signed transport document

- a bill of lading (often used for sea transport)

- an invoice issued by the goods transport company.

Alternatively, you can present one transport document and one of the following documents:

- an insurance policy relating to the dispatch or transportation of the goods, or banking documents confirming payment of transport or delivery of the goods

- official documents issued by a government agency confirming arrival of the goods in the EU country to which they were transported

- a receipt issued by a stockist in the EU country to which the goods were transported, confirming storage of the goods in that country.

If the buyer is responsible for transport, you must also have a written statement from them. This statement must confirm that the goods have been transported to the country of destination by the buyer or by a third party, such as an independent transport company, on the buyer’s behalf. The buyer must provide you with the statement no later than the 10th day of the month following delivery of the goods. It must contain the following details:

- the date on which the statement was issued

- the buyer’s name and address

- the quantity and nature of the goods

- the date and place of arrival of the goods

- the registration number (if you have sold a means of transport).

If another party receives the goods on the buyer’s behalf, you must also have a copy of that person’s ID.

Please note that you cannot apply the presumption rule if the buyer takes the goods to another EU country using their own means of transport, such as their private car.

Application of the presumption rule is optional, so it does not prevent you from using other documentary proof of transport.

Here’s how to prepare your VAT-exclusive sales invoices for goods sold within the EU

Specific invoicing rules apply when you sell goods to a buyer in another EU country who is obliged to report output VAT on their purchase.

You must issue the invoice no later than the 15th day of the month following the month during which the goods were delivered. In addition to the standard invoicing details, you must also include the following:

- the buyer’s VAT number

- one of the following references to explain why you haven't charged VAT on the sale:

- “Exempt from VAT” or “Exempt”

- “Chapter 10, Section 42 of the Swedish VAT Act”

- “Article 138 of the VAT Directive”

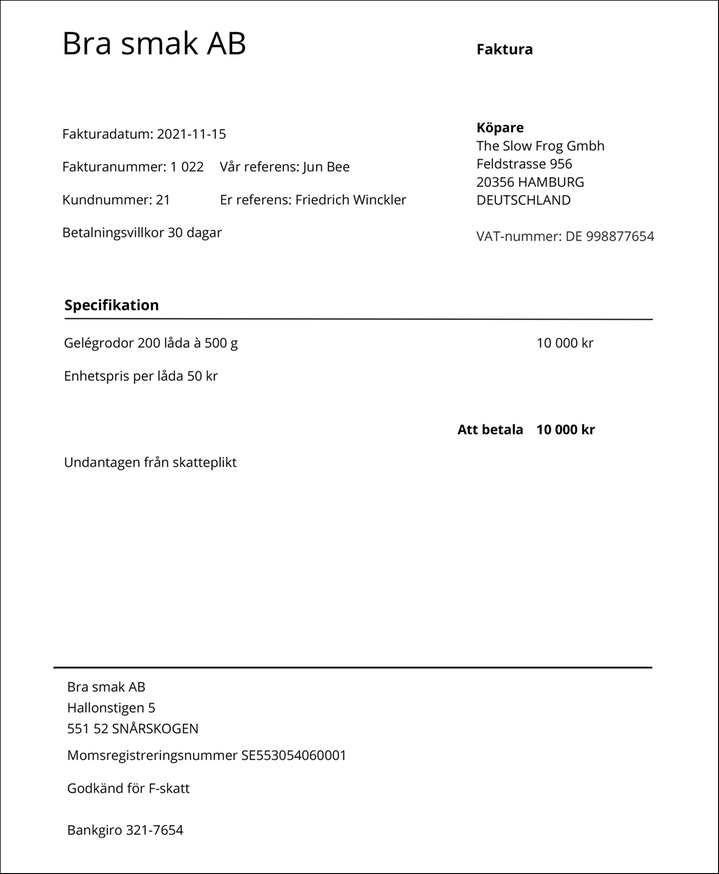

Example: invoice for VAT-exempt sale of goods within the EU

The image is an example of an invoice. This invoice relates to the VAT-exempt sale of goods to a VAT-registered buyer in another EU country.

On the invoice, you are required to state the buyer’s VAT number and a reference to explain why you haven't charged VAT. The reference provided in this example is: “Exempt from VAT”.

Here’s how to report VAT-exclusive sales of goods that you’ve made within the EU

When you make a VAT-exclusive sale of goods to a VAT-registered buyer in another EU country, the buyer must report the VAT in the other country. However, you still need to report the sale in your VAT return. To do this, enter the sales amount in Swedish kronor in box 35.

You must also provide details of the buyer’s VAT number and the sales amount in an EC sales list (recapitulative statement).

Example: reporting in a VAT return and EC sales list (recapitulative statement)

Kim’s business in Sweden sells a machine for SEK 100,000 to Fritz’s company in Germany. Kim and Fritz are both registered for VAT in their respective countries. Fritz will use the machine for business purposes. Kim hires an independent transport company to move the machine from Sweden to Germany.

Kim’s sale is exempt from VAT since the requirements for VAT-exempt sales of goods within the EU have been met.

Kim states both Fritz’s VAT number and his own on the invoice. Kim also refers to “Article 138 of the VAT Directive” to make it clear that the buyer must pay the VAT.

Here’s how Kim reports the transaction in his VAT return

- He enters the sales amount (SEK 100,000) in box 35.

Here’s how Kim reports the transaction in his EC sales list

- He enters Fritz’s VAT number in field marked “Buyer’s VAT number, including country code”.

- He enters the sales amount (SEK 100,000) in the field marked “Value of supplies of goods”.

This is when you must report the sale

When you sell goods to a VAT-registered buyer in another EU country, there are special rules that determine when you must report the sale in your VAT return and EC sales list (recapitulative statement). The reporting date depends on when you issue the invoice and when the goods are delivered. The same rules apply regardless of whether you use the cash accounting method or the accrual accounting method.

- You must report the sale in the period in which you issue the invoice to the buyer. You must issue the invoice no later than the 15th day of the month following the month during which the goods are delivered.

- If you issue the invoice late, you must still report the sale during the period that includes the 15th day of the month following the month of delivery.

- If you issue the invoice and receive payment before the goods have been delivered to the buyer (an advance payment), you must report the sale during the period in which the goods are delivered.

Examples of reporting dates in various circumstances

In this example, Kim’s company in Sweden sells goods to Fritz’s company in Germany. Kim and Fritz are both registered for VAT in their respective countries. Fritz will use the goods for business purposes. An independent transport company moves the goods from Sweden to Germany.

Kim files quarterly VAT returns and submits an EC sales list every month.

The invoice is issued during the month of delivery

Kim delivers the goods to Fritz in Germany on 11 March and issues the invoice on 17 March. In this case, the invoice is issued during the month in which the goods are delivered (March). This means that Kim must report the sale in his VAT return for January-March, and in his EC sales list for March.

The invoice is issued late

Kim delivers the goods to Fritz in Germany on 11 March but doesn’t issue the invoice until 17 May. In this case, the invoice is issued late, since the deadline was15 April. Kim must still report the sale in the period that includes the 15th day of the month following the month of delivery. He therefore reports the sale in his VAT return for April-June and in his EC sales list for April.

The invoice is issued before the delivery month (advance invoicing)

Kim delivers the goods to Fritz in Germany on 12 May but issues the invoice on 17 March. In this case, the invoice is issued in advance, i.e. before delivery. Here, the date of delivery determines the reporting date. Since the goods are delivered in May, Kim must report the sale in his VAT return for April-June and in his EC sales list for May.

Special regulations on chain transactions within the EU

In a chain transaction, goods are traded between three or more parties and transported from one EU country to another. The goods are transported directly from the initial seller to the final buyer in the chain.

In a chain transaction, it must be determined which sale the goods transport is linked to. The first seller, the final buyer, or the intermediary buyer in the chain transaction might be responsible for transporting the goods.

The general rule is that the goods transport is linked to the sale to the intermediary, if the intermediary is responsible for transport and has not provided a VAT number issued by the country of dispatch. However, there is also an exemption rule. Under this rule, if the intermediary is responsible for transporting the goods and has provided a VAT number issued by the country of dispatch, transport is linked to the sale made by the intermediary instead.

Examples: the general rule and the exemption rule

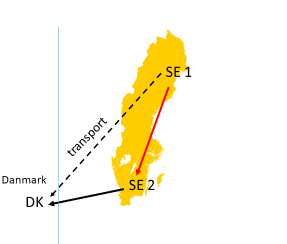

The general rule

The Swedish company SE1 sells goods to another Swedish company, SE2. SE2 resells the goods to a Danish company, DK. SE2 is VAT registered in both Sweden and Denmark. SE2 provides its Danish VAT number to SE1.

The goods are held by SE1 in Sweden, and SE2 is responsible for transporting them. The goods are transported directly from SE1 in Sweden to DK in Denmark.

In this case, SE2 has provided its Danish VAT number to the seller, SE1. Goods transport is therefore linked to SE1’s sale to SE2.

This sale is VAT exempt, provided that all the requirements for VAT-exempt sales of goods to other EU countries are met.

%20Kedjetransaktioner-exempel-huvudregeln.png)

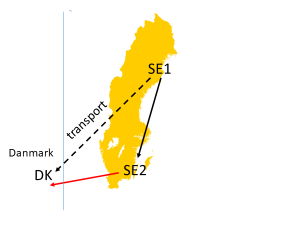

There is also an exemption rule: if the intermediary is responsible for transporting the goods and has provided a VAT number issued by the country of dispatch, goods transport is linked to the intermediary’s sale instead.

The exemption rule

If SE2 provides its Swedish VAT number to SE1, the transport is linked to SE2’s sale to DK instead.

This sale is exempt from VAT, provided that the other requirements for VAT-exempt sales of goods to other EU countries are met.

However, SE1’s sale to SE2 is subject to VAT, which means that SE1 must charge Swedish VAT and report it in its VAT return.

%20Kedjetransaktioner-exempel-undantagsregeln.png)

If the first company in the chain transaction (SE1 in both examples above) is responsible for transporting the goods, transport is linked to the first company’s sale. If the final company in the chain transaction (DK in both examples above) is responsible for transporting the goods, transport is linked to the final sale instead.

Triangulation

Triangulation is a form of chain transaction between three businesses that are VAT registered in three different EU countries. In this case, we’ll refer to the three businesses involved as A, B and C for simplicity. In this triangulation transaction, A sells goods to B, and B resells these goods to C.

However, the goods are transported directly from A to C. All three businesses in the chain must be registered for VAT in their respective EU countries for the transaction to qualify as a triangulation transaction. The third party in the chain (C) must be registered for VAT in the country to which the goods are transported. In a triangulation transaction, the first buyer in the chain (B) is known as the intermediary.

The way in which you report the sale and purchase of goods in a triangulation transaction is determined according to whether you’re the first, second or third party in the chain (A, B or C).

Here’s how to report VAT if you’re the first party in the chain (A)

If you’re the first party in the chain (A), and you’re registered for VAT in Sweden, you can sell the goods to your buyer (B) on a VAT-exempt basis if you meet certain conditions. B must be registered for VAT in a different EU country from you and must provide you with their VAT number. As the seller, you must also be able to prove that the goods have been transported to another EU country.

The invoice you issue to B must state B’s VAT number as well as your own.

You report the sale in box 35 of your VAT return.

You must also report the sale in your EC sales list (recapitulative statement).

Example

Maja’s company in Sweden sells a machine to Bastien’s company in Belgium for SEK 100,000. Bastien resells the machine to Ditte’s company in Denmark. All three companies are VAT registered in their respective countries. Maja delivers the machine directly from Sweden to Denmark.

Maja’s sale to Bastien is VAT exempt, since the conditions for VAT-exempt sales of goods to another EU country have been met.

Maja states both Bastien’s VAT number and her own on the invoice. Maja also specifies that the buyer must pay the VAT. She does this by referring to “Article 138 of the VAT Directive”.

Here’s how Maja reports the sale in her VAT return

- She enters the sales amount (SEK 100,000) in box 35.

Here’s how Maja reports the sale in her EC sales list (recapitulative statement)

- She enters Bastien’s VAT number in the field marked “Buyer’s VAT number”, including the country code.

- She enters the sales amount (SEK 100,000) in the field “Value of supplies of goods”.

Here’s how to report VAT as the second party in the chain: the intermediary (B)

If you’re the intermediary (B) and you’re registered for VAT in Sweden, you must not report any output VAT on your purchase from the seller (A). This rule applies if you can prove that you purchased the goods to resell them to C. C must also have provided you with their valid VAT number.

On your invoice to C, you must state both the buyer’s (C’s) VAT number and your own. You must specify that the invoice relates to a triangulation transaction, and you must also write “VAT reverse charge liability” on it.

You report your purchase of the goods in box 37 of your VAT return. You report your sale of these goods in box 38.

You must also report the sale in your EC sales list (recapitulative statement).

Example

Gina’s company in Germany sells goods for SEK 40,000 to John’s company in Sweden, which resells them for SEK 50,000 to Preben’s company in Denmark. All three companies are registered for VAT in their respective countries. Gina delivers the goods directly from Germany to Denmark.

In his invoice to Preben, John states Preben’s VAT number in addition to his own. He also states that the invoice relates to a sale as part of a triangulation transaction and writes “VAT reverse charge liability”.

John must not report or pay VAT on his purchase from Germany, but he must still report both the purchase price and his own sale price in his VAT return.

Here’s how John reports the transaction in his VAT return

- He enters the amount he paid for the goods (SEK 40,000) in box 37.

- He enters the amount he sold the goods for (SEK 50,000) in box 38.

Here’s how John reports the transaction in his EC sales list (recapitulative statement)

- He enters Preben’s VAT number in the field “Buyer’s VAT number”, including the country code.

- He enters the amount he sold the goods for (SEK 50,000) in the field “Value of triangulation transaction”.

Please note that the triangulation regulations do not apply unless you can prove that you purchased the goods from A to resell them to C. C must also be registered for VAT in a different EU country from both A and B. If you cannot prove this, you must report output VAT on the purchase from A under the rule known as the fallback rule.

Example: the fallback rule

Paul’s company in Germany sells a machine to Stina’s company in Sweden for SEK 40,000. Stina provides Paul with her Swedish VAT number. Stina asks Paul to send the machine from Germany to Hungary.

Stina does not have a VAT-registered buyer for the machine in Hungary, so the rules on triangulation do not apply to this transaction. Stina cannot prove that she has paid VAT on the purchase in Hungary either. She must therefore pay VAT in accordance with the fallback rule.

Under the fallback rule, Stina must calculate and report output VAT on the purchase in her Swedish VAT return – even though the machine has been transported to Hungary. In this case, the VAT amounts to SEK 10,000 (40,000 × 0.25). Stina is entitled to claim a deduction for the input VAT amount, if she can prove that the machine relates to her VAT-liable transactions in Sweden or other EU countries.

Here’s how Stina reports the transaction in her VAT return

- She enters the amount she paid for the machine (SEK 40,000) in box 20.

- She enters the output VAT on the machine (SEK 10,000) in box 30.

Here’s how to report VAT as the third party in the chain (C)

If you’re the third party in the chain and you’re registered for VAT in Sweden, you must report your purchase from B in box 20 of your VAT return. You must calculate the output VAT yourself, and report it in box 30, 31 or 32 as appropriate.

Example

Liam’s company in Sweden buys goods from Alina’s company in Romania. Liam pays SEK 100,000 for the goods, which includes a delivery charge of SEK 10,000. When he makes his purchase, Liam provides his Swedish VAT number to Alina. The goods are transported directly to Sweden from Alina’s supplier in Denmark. Alina does not charge VAT on the goods or delivery.

In this example, the goods are transported from a company in Denmark to Sweden. It does not actually matter which EU country outside Sweden the delivery is made from.

Since Liam has purchased the goods from another EU country, he must calculate the VAT himself and report it in his VAT return. Liam calculates VAT at 25% on the price of the goods including delivery, i.e. SEK 100,000. Since Liam will use the goods for VAT-liable business purposes, he can claim a deduction for the VAT amount that he’s calculated.

Here’s how Liam reports the transaction in his VAT return

- He enters the amount he paid for the goods including delivery (SEK 100,000) in box 20.

- He enters the output VAT he has calculated on the purchase (SEK 25,000) in box 30.

- He enters the deduction amount for input VAT (SEK 25,000) in box 48.

Special regulations regarding certain sales and transfer of goods within the EU

Special regulations apply to the sale of certain goods, and the transfer of goods within the EU.

- Supply of goods with installation or assembly services (in Swedish)

- Electricity, gas, heating and cooling (in Swedish)

- Transfer of goods between EU countries (in Swedish)

Selling goods to private individuals within the EU

Special regulations also apply if you sell goods to buyers not making intra-Community acquisitions, such as private individuals.

Ansök om att redovisa distansförsäljning i One Stop Shop (OSS)